Research

Kalshi vs Polymarket: Which Prediction Market is Better in 2026?

Kalshi closed a $22B Series F on May 7, 2026. Polymarket reached $15B in March. Both hold CFTC licenses, but their fees, US accessibility, and category coverage diverge sharply. Here's where each platform wins.

TL;DR

- Kalshi: $22B valuation, $14.81B April 2026 volume (+13.3% MoM), accessible in 49 states + DC (banned in Nevada).

- Polymarket: $15B valuation secured March 2026, $9B April Global volume (−14.8% MoM), 50-state CFTC license but invite-only US beta with a 1M+ waitlist.

- Fees on 100 contracts at $0.50: Kalshi $1.75 / Polymarket Global Politics $1.00 / Polymarket Global Geopolitics $0.00.

- DropsTab data tracks Kalshi PreStocks at -53 VWAP and Polymarket PreStocks at -71 — both Undervalued in secondary markets despite record primary valuations.

- Cross-venue arbitrage: 2–5% spreads documented on major events; World Cup 2026 outright winners trade 1.3pp apart on France.

- 1. Kalshi vs Polymarket: Quick Verdict

- 2. Kalshi vs Polymarket Volume and Valuation in 2026

- 3. Kalshi vs Polymarket Fees: What Traders Actually Pay

- 4. US Accessibility and Regulatory Status (May 2026)

- 5. Market Coverage and Category Depth

- 6. Kalshi vs Polymarket Arbitrage Opportunities

- 7. POLY Token Launch and Fee Disruption (Q2 2026)

- 8. Which Is Better in 2026? Decision Framework

Kalshi vs Polymarket: Quick Verdict

Kalshi and Polymarket together capture 85–95% of prediction-market sector volume, but they are not the same product. Kalshi is a CFTC-regulated USD-native exchange with $14.81B in April 2026 monthly volume and a sports-led model. Polymarket runs two products — an offshore USDC-on-Polygon platform and a CFTC-licensed US beta — with deeper non-sports coverage and lower fees on most categories.

The 2026 picture flipped from 2025. Polymarket led on monthly volume for most of 2025; Kalshi — led by CEO Tarek Mansour and COO Luana Lopes Lara — pulled ahead in Q1 2026 and widened the gap in April. According to DropsTab fundraising data, Kalshi raised across Seed → Series F totaling roughly $2.6B in equity, plus $300M in debt financing — $2.9B in cumulative capital. Polymarket fundraising shows ICE alone has committed $2B since October 2025.

Kalshi vs Polymarket Volume and Valuation in 2026

Kalshi processed $14.81B in April 2026 notional volume — a 13.3% jump over March and the platform's highest month on record despite no Super Bowl, March Madness, or NFL playoff games on the calendar. Polymarket Global moved $9B in the same month, a 14.8% decline from March. The two platforms now control 85–95% of sector volume combined.

Kalshi's funding trajectory has been the fastest among prediction-market venues. The platform raised a $185M Series C at $2B led by Paradigm in June 2025, then hit $5B in October 2025 (Series D, a16z and Sequoia co-leading), $11B in December 2025 (Series E, Paradigm leading a second time), and $22B on May 7, 2026 — Coatue led the latest round with Sequoia, Andreessen Horowitz, IVP, Paradigm, Morgan Stanley, and ARK Invest participating. Paradigm's three-round conviction across Series C, E, and F — leading two of them — is the strongest single-fund commitment in the prediction-market sector.

Polymarket's $9B post-money in October 2025 came from ICE's $2B Series D commitment (with $1B deployed as initial tranche; the remaining $600M followed in March 2026).; ICE doubled down with a $600M direct investment on March 27, 2026, and an additional $400M is in talks at the same $15B level.

| Metric | Kalshi | Polymarket Global | Polymarket US |

|---|---|---|---|

| Valuation (May 10, 2026) | $22B | $15B (secured Mar 2026) | Same legal entity |

| 2024 notional volume | ~$300M | ~$16.3B | n/a (US relaunched Dec 2, 2025) |

| 2025 notional volume | $22.88B | $33.4B | n/a |

| April 2026 volume | $14.81B | $9.0B | $1.26B |

| April 2026 MoM | +13.3% | −14.8% | n/a |

| YTD 2026 (through Apr 20) | ~$37.49B | ~$29.23B (Global + US combined) | included |

| Open interest (May 1, 2026) | $630.7M | $449.9M | included |

| Annualized run-rate | $178B | not disclosed | not disclosed |

Source: Dune Analytics, Sacra, Kalshi Series F release, as of May 10, 2026

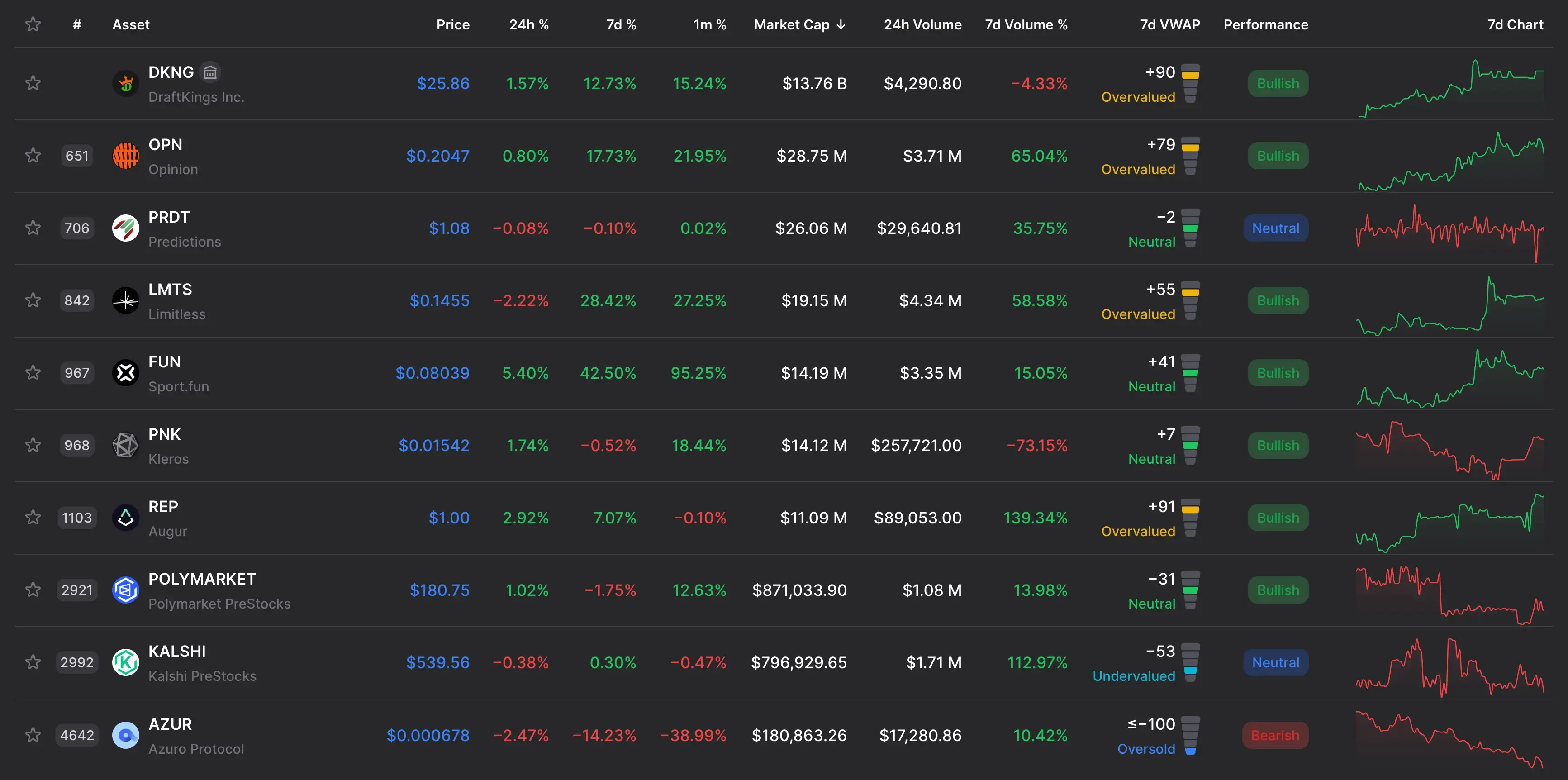

The static valuation picture tells one story. The live secondary market tells another. DropsTab data tracks Kalshi PreStocks at $538.32 with a -53 VWAP signal (Undervalued) and Polymarket PreStocks at $179.26 with -71 — both Undervalued in secondary readings even as their primary valuations hit $22B and $15B.

DraftKings (DKNG), the closest public-market proxy, is up 13.51% over the past month with a +90 VWAP score (Overvalued) at a $13.53B market cap. The TradFi sportsbook leg is being priced for the same secular flow, but harder than either prediction-market PreStock.

Sacra primary research shows Kalshi generated $260M in 2025 revenue against $22.88B in trading volume — a 1.14% take rate while Polymarket only began monetizing in Q1 2026. That asymmetric revenue picture is the cleanest explanation for the $7B valuation gap.

The category split inside those volume numbers matters more than the totals. As crypto-finance analyst Spencer Bogart noted on April 26, 2026:

"Kalshi and Polymarket were nearly tied on total volume in March at ~$12B each. Strip out sports and it's a different picture. Polymarket did $7.5B in non-sports volume. Kalshi did $1.6B." That's the real divergence — two platforms competing in the same league for top-line dollars but on entirely different products underneath.

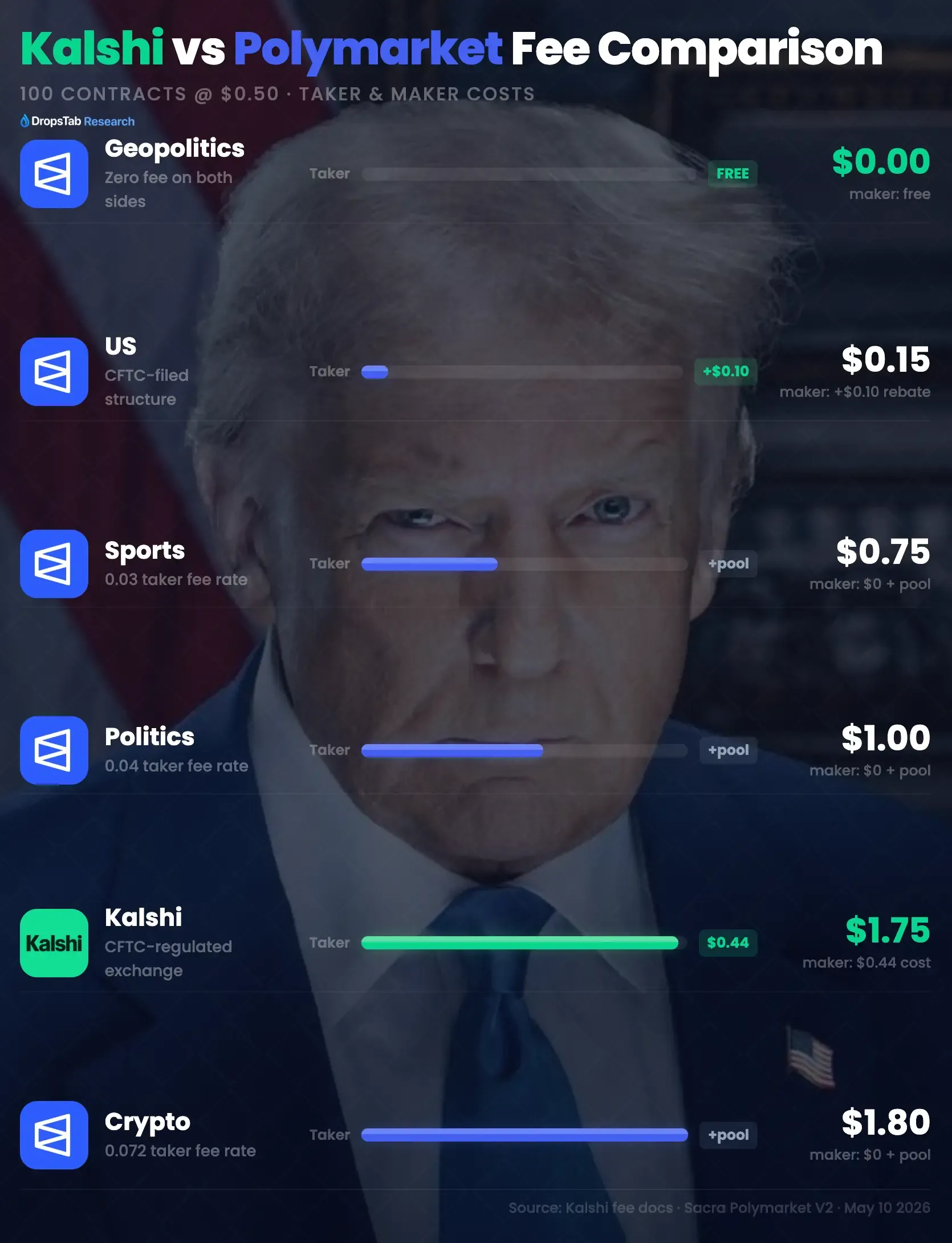

Kalshi vs Polymarket Fees: What Traders Actually Pay

Polymarket Global charges zero fees on geopolitics markets for both makers and takers, while Kalshi's parabolic fee structure peaks at 3.5% of contract premium at the $0.50 price point — a 30–60% cost advantage for Polymarket on mid-priced contracts in most categories. Kalshi's structural defense is a 3.75–4% variable APY on idle balances, which Polymarket does not offer.

Kalshi uses a parabolic fee structure: taker fee = 0.07 × C × p × (1 − p), capped at $1.75 per 100 contracts; maker fee = 0.0175 × C × p × (1 − p), capped at $0.4375. Polymarket Global moved to per-category taker fees on March 30, 2026, with maker fees at zero plus a 20–50% rebate share from the daily Maker Rebates pool.

| Trade: 100 contracts @ $0.50 | Taker cost | Maker cost / rebate |

|---|---|---|

| Kalshi | $1.75 | $0.4375 (paid) |

| Polymarket Global Sports (0.03) | $0.75 | $0 + 25% rebate pool share |

| Polymarket Global Politics (0.04) | $1.00 | $0 + 25% rebate pool share |

| Polymarket Global Crypto (0.072) | $1.80 | $0 + 20% rebate pool share |

| Polymarket Global Geopolitics | $0.00 | $0.00 |

| Polymarket US (filed CFTC structure) | 30 bps taker | 20 bps maker rebate |

Source: Kalshi fee docs, Sacra Polymarket V2 schedule, DeFi Rate, as of May 10, 2026

The structural counter on Kalshi is the 3.75–4% variable APY on cash and open positions — a fee-equivalent yield that tracks the Fed funds rate. On a $10,000 balance, that generates roughly $33 per month in interest before compounding. Polymarket pays 0% on idle balances on either product. For event-level scale: Kalshi generated $8.7M in fees on Super Bowl 2026 alone. Both venues materially undercut traditional sportsbook vig of 4–6% standard and 15–20% on parlays.

A note on Polymarket US specifically: a 50% taker rebate was active through April 30, 2026, halving the effective rate on its 30-bps base structure. As of May 10, 2026, no public extension announcement has been issued — assume expired unless verified through Polymarket US channels directly.

US Accessibility and Regulatory Status (May 2026)

Federal preemption arguments have won at the federal court level — Arizona, New Jersey, and Tennessee all sided with the CFTC against state regulators in 2026. State courts have moved the other way, with Nevada becoming the only state with an active court-enforced ban on Kalshi as of May 2026. The split sets up a Supreme Court resolution that TD Cowen analysts forecast may not arrive until 2028.

On May 5, 2026, Arizona federal Judge Michael Liburdi blocked the state's criminal prosecution of Kalshi on federal preemption grounds — the third federal court to side with the CFTC over a state regulator in 2026 alone. The Massachusetts injunction granted in January was stayed pending appeal in February. Nevada Judge Jason Woodbury granted a preliminary injunction on April 3, 2026, with Kalshi required to implement geofencing by May 4. The 3rd Circuit ruled in Kalshi's favor on April 6, 2026 in a similar New Jersey dispute. The 9th Circuit heard oral arguments on April 16 and a ruling is pending.

| State | Kalshi status | Polymarket US status |

|---|---|---|

| Massachusetts | Injunction stayed pending appeal | Available |

| Nevada | Active court-enforced ban (only state) | Reportedly restricted |

| Arizona | Federal preemption granted (May 5, 2026) | Available |

| New Jersey | 3rd Circuit ruled for Kalshi (April 6, 2026) | Available |

| Tennessee | Federal preliminary injunction (Feb 2026) | Available |

| New York | Active enforcement | Reportedly restricted |

| Washington | Lawsuit filed March 27, 2026 | Available |

| MD, OH, MI, IA, UT, OR, IL, CT | Active state enforcement | Available |

| All other states + DC | Available (49 + DC) | 50-state CFTC license but invite-only beta |

Source: Court filings, CFTC, Kalshi activities feed on DropsTab, as of May 10, 2026

CFTC Chair Mike Selig has publicly defended federal jurisdiction; the agency sued Arizona, Connecticut, and Illinois directly in late April 2026. 38 state AGs signed an amicus brief supporting Massachusetts on April 27, 2026. The two Polymarket products differ structurally: Polymarket Global (offshore Polymarket Inc.) remains geo-blocked from US users since the 2022 CFTC settlement. Polymarket US (QCX LLC) holds the CFTC DCM license obtained via the $112M QCEX acquisition in July 2025 and the Amended Order of Designation issued November 25, 2025.

Market Coverage and Category Depth

| Metric | Kalshi | Polymarket Global | Polymarket US |

|---|---|---|---|

| Active markets | 350,000+ | 1,600+ Politics, 157 Economy + others | Sports-led at launch |

| Sports % of volume | 84–90% (89% of 2025 revenue) | ~46% (April 2026) | ~100% at launch |

| Distinctive categories | Mention markets, Build Your Combo parlays, FOMC, weather | Geopolitics (fee-free), nuclear odds, conflict timelines | Sports first; broader rollout in progress |

| Resolution | Designated third-party sources | UMA optimistic oracle | UMA / official sources |

| Position limits | $25,000 default; $7M select | None (liquidity-bound) | None (liquidity-bound) |

Source: Sacra, Kalshi official data, as of May 10, 2026

Kalshi lists 350,000+ active markets, with sports accounting for 84–90% of volume — 89% of 2025 fee revenue per Sacra primary data. The platform's mention markets, launched in fall 2025 with parlays added November 2025, peaked at $3.55M per-game NFL volume during conference championships. Major channel partners include Robinhood (>50% of Kalshi 2025 volume), CNN, CNBC, the NHL, and Coinbase.

Polymarket Global runs a more distributed category mix. April 20 week breakdown: Sports 46%, Crypto 22%, Politics 27% — non-sports volume sits at roughly 54%. Politics alone has 1,600+ active markets. Major partnerships include ICE (data plus tokenization), MetaMask (December 2025), Jupiter (February 2026), and MLB (March 2026 — "Official Prediction Market Exchange Partner" with Sportradar data integration). Polymarket US continues sports-led rollout; broader category expansion is in progress per Coplan but not confirmed in primary sources for April 2026.

DropsTab data also tracks the on-chain prediction-market infrastructure layer that historically settled markets — Augur (REP) at $0.9595 trades flat at -0.97% over the past month, Azuro (AZUR) is down 36.95%, and Kleros (PNK) is up 15.89% with an Oversold reading. None of these tokens has reactivated meaningfully despite the Kalshi/Polymarket boom — a signal that the duopoly is consolidating value at the venue layer rather than the protocol layer.

Kalshi vs Polymarket Arbitrage Opportunities

Cross-venue spreads are documented and persistent. World Cup 2026 outright winner odds trade 1.3pp apart on France between Kalshi and Polymarket as of May 4, 2026, with sustained 5–8 cent gaps on individual team contracts. General arbitrage commentary places typical gaps at 2–5% on major events — but capital-allocation friction prevents fully clean execution.

DeFi Rate's May 4, 2026 snapshot shows the persistent spread structure on World Cup 2026 outright winners:

| Team | Kalshi YES (implied %) | Polymarket Global YES (implied %) | Spread |

|---|---|---|---|

| France | 18.0% | 16.7% | 1.3 pp |

| Spain | 16.6% | 15.4% | 1.2 pp |

| England | 11.2% | 11.1% | 0.1 pp |

Source: DeFi Rate, as of May 4, 2026

Sustained 5–8 cent gaps on individual team contracts have been described by Oddpool as "one of the largest sustained spreads in prediction markets." The LA Mayoral election in February 2026 produced a clean cross-venue arb: YES on Kalshi at 58¢ + NO on Polymarket at 35¢ = 93¢ combined, gross 7.53% return per pair.

Execution friction is material. Kalshi withdrawals require 3 days for debit, 7 days for same-bank ACH, and up to 30 days for cross-bank — capital is locked across the spread window. Polymarket Polygon withdrawals are near-instant. Polymarket's tighter Global spreads (2–5¢) versus Kalshi's (3–8¢) reflect higher liquidity; closing equivalent 60-second VWAP requires roughly 3.5× more notional on Polymarket. Resolution-source asymmetry — Kalshi mention markets settle on official transcripts, Polymarket on broadcast or oracle subjectivity — creates basis risk that prevents fully clean execution even when prices diverge.

To run cross-venue arb you'll need accounts on both: Kalshi for the regulated USD leg, Polymarket for the offshore USDC leg.

For traders running this strategy, see the full Polymarket trading playbook.

Track Polymarket odds via DropsBot. This integration handles the alert and routing layer for cross-venue tracking through Telegram.

POLY Token Launch and Fee Disruption (Q2 2026)

Polymarket CMO Matthew Modabber confirmed a token and airdrop on October 24, 2025 — sequencing places launch after the US relaunch stabilizes. No tokenomics document, supply figure, or fee discount tier has been published by Polymarket Foundation as of May 10, 2026. Industry consensus places the launch within the 2026 calendar year, but no Q2 2026 date has been verified.

Founder Shayne Coplan teased the launch in early October 2025; CMO Matthew Modabber confirmed it on the Degenz Live podcast: "There will be a token, there will be an airdrop."

Trademark filings for "POLY" and "$POLY" have been submitted. Tokenomics figures circulating in secondary coverage — a 5–10% airdrop allocation, fee discount tiers tied to staked balances — are unverified by primary source and should be treated as speculation.

Polymarket Global already undercuts Kalshi by 30–60% on mid-priced contracts (30–70¢) across most categories before any token-based discount. A confirmed POLY-based discount tier would entrench the cost advantage. Kalshi's primary structural defense remains the 3.75–4% APY on balances, not per-trade fee parity. Until POLY launches, the closest tradable proxy is the Polymarket PreStocks market on DropsTab, trading at $179.26 with a -71 VWAP signal heading into Q2 2026.

Which Is Better in 2026? Decision Framework

The Kalshi vs Polymarket which is better 2026 question has no single answer — six clean answers depending on workflow, category, and state. The two platforms are not running the same race despite top-line volume parity.

Bogart's framing from April 2026 is the cleanest summary: "It's weird that they're even in the same category given very different positioning for what prediction markets become." The decision tree:

- US retail in non-banned states with fiat workflows: Kalshi — USD-native rails, APY on balance, deeper sports liquidity, 1099 tax reporting, 350,000+ markets with regulated resolution sources.

- Mid-priced (30–70¢) contracts in politics, crypto, geopolitics, or culture: Polymarket Global — 30–60% cheaper. Geopolitics is fee-free and strictly dominant.

- Cross-venue arbitrage: Both required. 2–5% gaps on major events; 5–8¢ persistent on World Cup. Pre-fund both; account for Kalshi's 3–30 day withdrawal hold and Polymarket's resolution-basis risk.

- Regulatory durability: Kalshi's federal-preemption track record (3rd Circuit, AZ federal court, TN federal court) is strengthening, but Nevada plus Massachusetts pending appeal create persistent state-level surface area. Polymarket US has the same CFTC posture and a cleaner state-conflict record but is gated by a 1M+ waitlist.

- Airdrop / token-asymmetric upside: Polymarket only — POLY launch confirmed for the 2026 calendar year; trade history likely matters for airdrop allocation per Modabber's comments.

- Institutional flow: Kalshi annualized $178B run-rate with 800% institutional volume growth in six months — institutional default.

Ready to test the comparison? Sign up on Kalshi (49 states + DC, USD rails, APY on balance) or try Polymarket (USDC on Polygon, fee-free geopolitics, cross-venue arb).

Bernstein analysts project prediction-market sector volumes reaching $1T by 2030 — roughly 80% CAGR from a 2025 base of $51B, with 2026 pacing toward $240B. Kalshi and Polymarket capture 85–95% of that flow combined. The duopoly's $22B and $15B private valuations place both inside the upper tier of online-betting-industry equity value, even before token-based market cap is considered for Polymarket.

Disclosure: DropsTab may receive compensation when readers sign up via referral links in this article. Compensation does not affect editorial coverage, data accuracy, or competitive analysis.